Last week, Lakshman Achuthan of the Economic Cycle Research Institute (ECRI) made the rounds on financial television once again to discuss the current state of their recession call from late last year. Achuthan reaffirmed their belief that a return to economic contraction is likely in 2012, noting that the coincident data used to officially define economic cycle boundaries continue to signal slowing growthYes, U.S. GDP is still rising, according to the latest reports. But that doesn't mean we've dodged a new recession. Sound surprising? What most people don't understand is that recessions often begin when gross domestic product is still showing positive growth. Four of the past six recessions started during a quarter when GDP was growing, as did 72% of all recessions in the past 94 years.How can that be? The answer is that expansions end - and recessions begin - at the peak of the business cycle, after which the economy begins to contract. For instance, the initial quarter of the Great Recession of 2007-09 showed 1.7% GDP growth, while the severe 1973-75 and 1981-82 recessions began with 3.9% and 4.9% GDP growth, respectively. Revisions are another issue, so GDP could be contracting and we wouldn't know it for some time. That's why real-time data often doesn't show GDP turning negative until about half a year after the recession has actually begun - that's typically been the case in the past six recessions.It took more than a year to learn that GDP actually shrank by 1.3% during the first quarter of the 2001 recession. But back then, it was initially reported as having grown at 2.0%. That's not very different from the latest reading for GDP growth in the first quarter of 2012: 2.2%. In August 2008 - just before the Lehman collapse - GDP was reported to have risen in the first and second quarters with the latter revised up sharply, triggering over a 200-point rally in the Dow that day. Today we know that GDP actually shrank in the first quarter while the second has been revised down by two full percentage points. In the end, even if we don't see two successive down quarters of GDP, which is commonly believed to define a recession, that doesn't mean we've skirted one. That's only a rough rule of thumb, not an actual recession definition. In fact, two of the last 8 recessions did not contain two straight quarters of negative GDP.Confusion around what constitutes a recession is so common that we've gone into the details every time one appears on our radar screen. The last time we wrote about it was four years ago, in May 2008, when many still doubted our recession call. As we explained at the time, there are four key elements to consider: output, which includes GDP, but also employment, income and sales. One reason we believe the economy is heading for recession now is weak job growth. Since February, job growth has turned down, as have other key indicators. Ominously, in the past 60 years we haven't seen a slowdown where year-over-year job growth has dropped this low without recession. Separately, for the past three months, year-over-year growth in real personal income has stayed lower than it was at the start of each of the last ten recessions. These are facts, not forecasts - so the popular story that more jobs will lead to more consumption is missing a key link, which is income growth.In fact, our research shows a new recession is likely to start by mid-2012. Under the circumstances, complacency about U.S. recession risk is likely to prove badly misplaced.

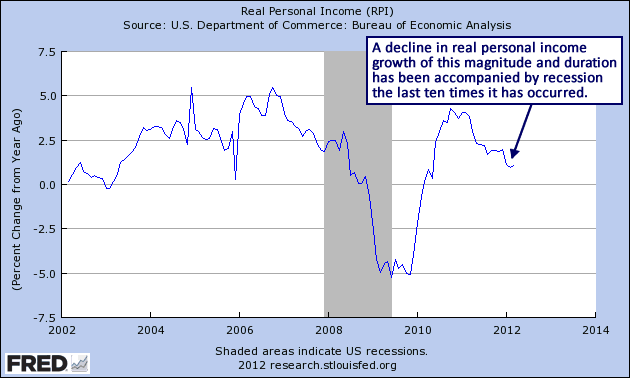

The decline in year-over-year growth in real personal income noted by Achuthan is displayed on the following graph from the Federal Reserve Economic Data (FRED) web site. A drop of this magnitude and duration has been accompanied by recession the last ten times it has occurred.

click to enlarge images

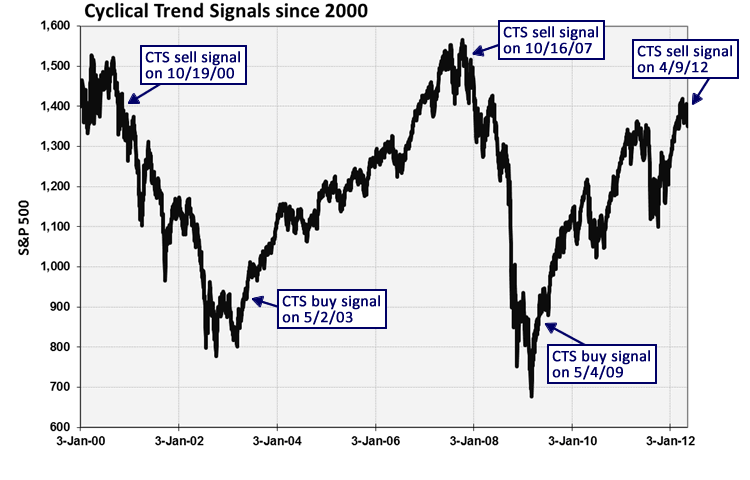

The mainstream view remains that a return to economic contraction in 2012 is not a viable scenario worth seriously considering. Only a few high-profile analysts, such as the folks at the ECRI and Hussman Funds, have maintained that the development of a recession is likely. Our own long-term computer models, which analyze a large basket of fundamental, internal, technical and sentiment data, also continue to favor the recession scenario and our Cyclical Trend Score (CTS) issued a sell signal in early April, indicating that the development of a cyclical bear market in stocks is highly likely.

As always, there are no certainties in the realm of financial market forecasting, only possible scenarios and their associated probabilities. However, the most reliable leading data continue to suggest that a return to economic contraction is likely in 2012. If the recession scenario does unfold as expected, the mainstream view will be forced to adjust eventually, but well after the fact, as usual.

No comments:

Post a Comment

Agrega tu comentario u opinión. Add your comment.

Si deseas puedes usar perfil anónimo o identificarte.